Microeconomics

$169.00

This product is currently sold out.

Microeconomics

Combined with Macroeconomics , Microeconomics completes a one-year curriculum. Our Economics course is simply a combination of both Microeconomics and Macroeconomics .

Our complete Microeconomics package includes:- 12-month Online Subscription to our complete Microeconomics course with video lessons, automatically graded problems, and much more.

- Printed Notes (optional) are the Microeconomics course notes from the Online Subscription printed in a color, on-the-go format.

Microeconomics Materials

Online Subscription, 12-month access

Access to a complete online package that includes everything you need.

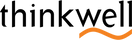

- Thinkwell's video lectures cover the comprehensive scope and sequence of topics covered in a college introductory microeconomics course.

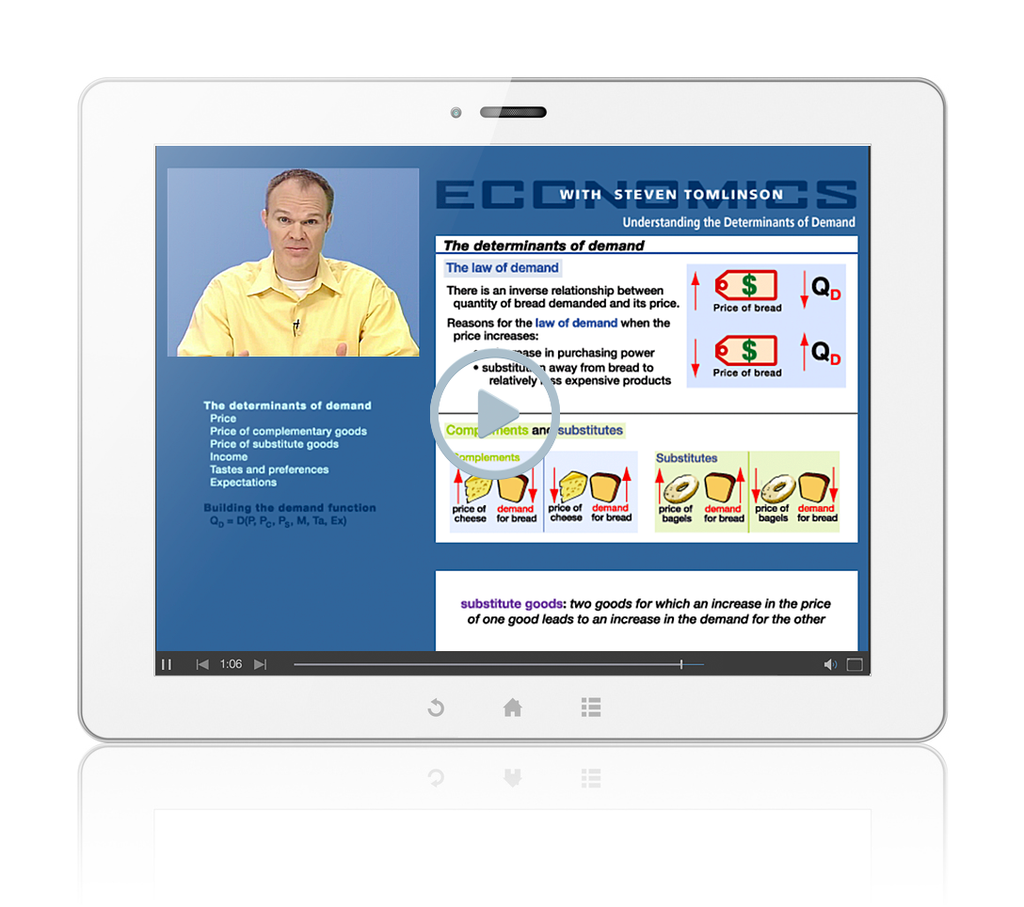

- Our automatically graded exercises with immediate feedback allow you to quickly determine which areas you'll need to spend extra time studying.

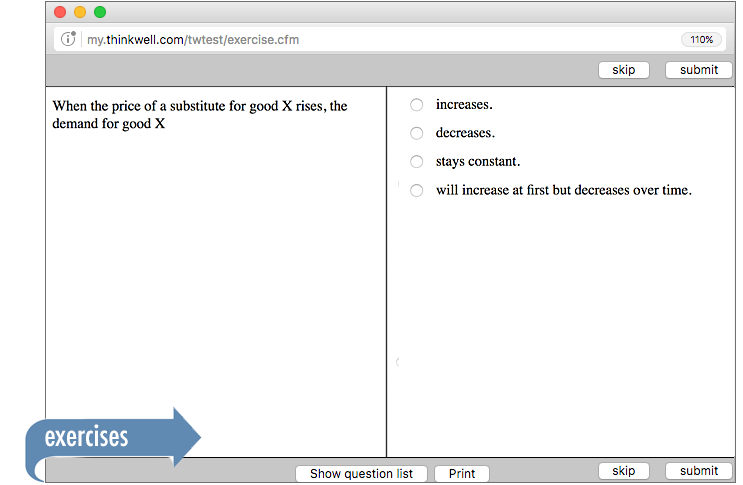

- Concise, illustrated review notes help you distill the fundamental ideas, concepts, and formulas you'll need to know in order to succeed.

- Subscriptions start when you are ready. Buy now and activate your course anytime you like. Wait up to one year to activate your subscription; your 12-month subscription doesn't begin until you say so!

Microeconomics Details

Thinkwell's Microeconomics includes:

- More than 130 topics with 170+ educational video lessons

- 1000+ interactive microeconomics exercises with immediate feedback allow you to track your progress

- Printable illustrated notes for each topic

- Glossary of 300 microeconomics terms

- Engaging content to help students advance their knowledge of economics:

- Supply, demand, equilibrium, and elasticity

- Consumer choice

- Production and costs

- Competitive markets and monopolies

- Resource markets

- Uncertainty, externalities, and market failure

- International trade

Table of Contents

1. Introduction to Economic Thinking

- 1.1 Basic Economics Ideas

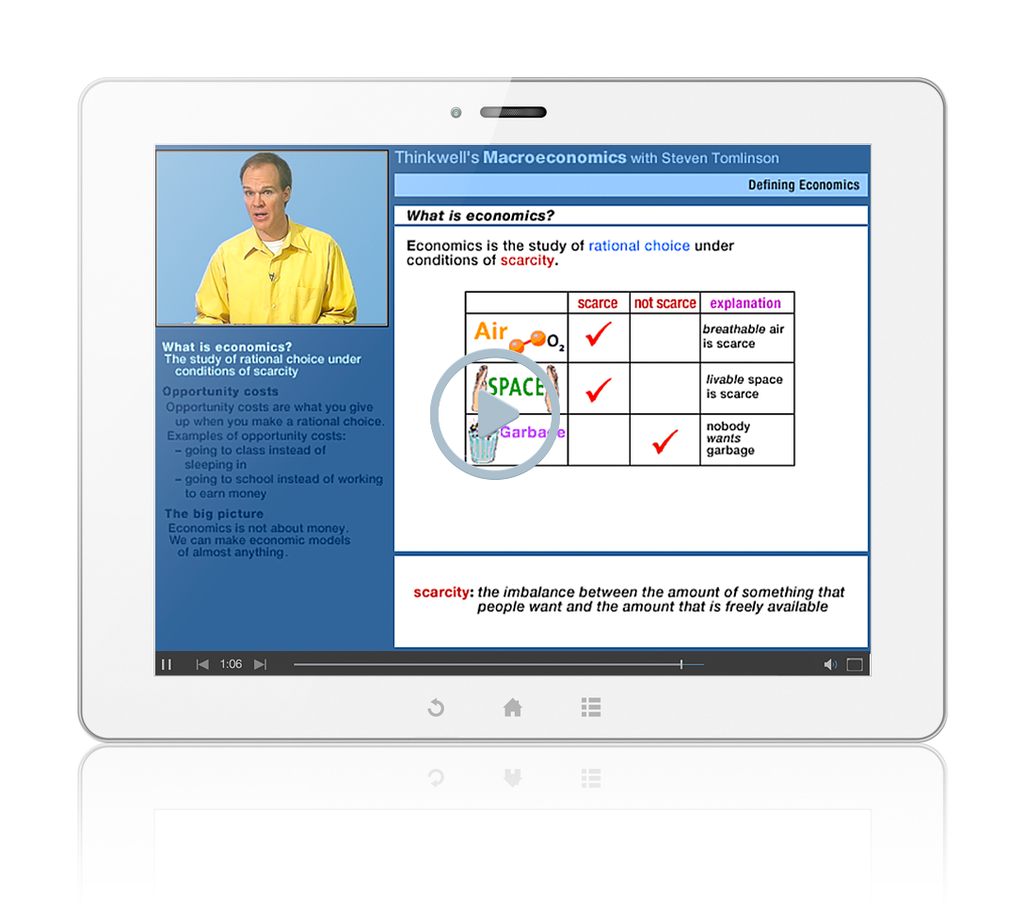

- 1.1.1 Defining Economics

- 1.1.2 Understanding the Concept of Value

- 1.2 Using Graphs

- 1.2.1 Using Graphs to Understand Direct Relationships

- 1.2.2 Plotting a Linear Relationship between Two Variables

- 1.2.3 Changing the Intercept of a Linear Function

- 1.2.4 Understanding the Slope of a Linear Function

- 1.3 Advanced Graphical Concepts

- 1.3.1 Understanding Tangent Lines

- 1.3.2 Working with Three Variables on a Graph

- 1.4 Production Possibilities

- 1.4.1 Understanding the Concept of Production Possibilities Frontiers

- 1.4.2 Understanding How a Change in Technology or Resources Affects the PPF

- 1.4.3 Deriving an Algebraic Equation for the Production Possibilities Frontier

- 1.5 Comparative Advantage

- 1.5.1 Defining Comparative Advantage with the Production Possibilities Frontier

- 1.5.2 Understanding Why Specialization Increases Total Output

- 1.5.3 Analyzing International Trade Using Comparative Advantage

- 1.5.4 Outsourcing

2. Understanding Markets

- 2.1 Demand

- 2.1.1 Understanding the Determinants of Demand

- 2.1.2 Understanding the Basics of a Demand Curve

- 2.1.3 Analyzing Shifts in the Demand Curve

- 2.1.4 Changing Other Demand Variables

- 2.1.5 Deriving a Market Demand Curve

- 2.2 Supply

- 2.2.1 Understanding the Determinants of Supply

- 2.2.2 Deriving a Supply Curve

- 2.2.3 Understanding a Change in Supply versus a Change in Quantity Supplied

- 2.2.4 Analyzing Changes in Other Supply Variables

- 2.2.5 Deriving a Market Supply Curve from Individual Supply Curves

- 2.3 Equilibrium

- 2.3.1 Determining a Competitive Equilibrium

- 2.3.2 Defining Comparative Statics

- 2.3.3 Classifying Comparative Statics

- 2.4 Elasticity

- 2.4.1 Defining Elasticity

- 2.4.2 Calculating Elasticity

- 2.4.3 Applying the Concept of Elasticity

- 2.4.4 Identifying the Determinants of Elasticity

- 2.4.5 Understanding the Relationship between Total Revenue and Elasticity

- 2.5 Interfering with Markets

- 2.5.1 Understanding How Price Controls Damage Markets

- 2.5.2 Understanding the Problem of Minimum Wages in Labor Markets

- 2.5.3 Understanding How an Excise Tax Affects Equilibrium

- 2.6 Agriculture Economics

- 2.6.1 Examining Problems in Agricultural Economics

3. Consumer Choice and Household Behavior

- 3.1 Utility Theory

- 3.1.1 Understanding Utility Theory

- 3.1.2 Finding Consumer Equilibrium

- 3.2 Budget Constraints and Indifference Curves

- 3.2.1 Constructing a Consumer's Budget Constraint

- 3.2.2 Understanding a Change in the Budget Constraint

- 3.2.3 Understanding Indifference Curves

- 3.3 Consumer Optimization

- 3.3.1 Locating the Consumer's Optimal Combination of Goods

- 3.3.2 Understanding the Effects of a Price Change on Consumer Choice

- 3.3.3 Deriving the Demand Curve

4. Production and Costs

- 4.1 The Basics of Production

- 4.1.1 Understanding Output, Inputs, and the Short Run

- 4.1.2 Explaining the Total Product Curve

- 4.1.3 Drawing Marginal Product Curves

- 4.1.4 Understanding Average Product

- 4.1.5 Relating Costs to Productivity

- 4.2 Variable Costs

- 4.2.1 Defining Variable Costs

- 4.2.2 Graphing Variable Costs

- 4.2.3 Graphing Variable Costs Using a Geometric Trick

- 4.3 Marginal Costs

- 4.3.1 Defining Marginal Costs

- 4.3.2 Deriving the Marginal Cost Curve

- 4.3.3 Understanding the Mathematical Relationship between Marginal Cost and Marginal Product

- 4.4 Average Costs

- 4.4.1 Defining Average Variable Costs

- 4.4.2 Understanding the Relationship between Average Variable Cost and Average Product of Labor

- 4.4.3 Understanding the Relationship between Marginal Cost and Average Variable Cost

- 4.5 Total Costs

- 4.5.1 Defining and Graphing Average Fixed Cost and Average Total Cost

- 4.5.2 Calculating Average Total Cost

- 4.5.3 Putting the Cost Curves Together

- 4.6 Long-Run Production and Costs

- 4.6.1 Defining the Long Run

- 4.6.2 Determining a Firm's Returns to Scale

- 4.6.3 Understanding Short-Run and Long-Run Average Cost Curves

- 4.6.4 Shifts in Cost Curves

- 4.7 Isocost/Isoquant Analysis

- 4.7.1 Constructing Isocost Lines

- 4.7.2 Understanding Isoquants

- 4.7.3 Finding the Cost-Minimizing Combination of Capital and Labor

5. Perfect Competition

- 5.1 The Basic Assumptions of Competitive Markets

- 5.1.1 Calculating Total Revenue

- 5.1.2 Understanding the Role of Price

- 5.1.3 Understanding Market Structures

- 5.1.4 Finding Economic and Accounting Profit

- 5.2 Calculating Profit and Loss

- 5.2.1 Finding the Firm's Profit-Maximizing Output Level

- 5.2.2 Proving the Profit-Maximizing Rule

- 5.2.3 Calculating Profit

- 5.2.4 Calculating Loss

- 5.2.5 Finding the Firm's Shut-Down Point

- 5.3 Market Supply

- 5.3.1 Deriving the Short-Run Market Supply Curve

- 5.3.2 Relating the Individual Firm to the Market

- 5.3.3 Examining Shifts in the Short-Run Market Supply Curve

- 5.3.4 Deriving the Long-Run Market Supply Curve

- 5.4 Competitive Firms' Responses to Price Changes

- 5.4.1 Examining the Firm's Long-Run and Short-Run Adjustments to a Price Increase

6. Other Market Models

- 6.1 Monopolies

- 6.1.1 Defining Monopoly Power

- 6.1.2 Defining Marginal Revenue for a Firm with Market Power

- 6.1.3 Determining the Monopolist's Profit-Maximizing Output and Price

- 6.1.4 Calculating a Monopolist's Profit and Loss

- 6.1.5 Graphing the Relationship between Marginal Revenue and Elasticity

- 6.2 The Social Cost of Monopoly

- 6.2.1 Determining the Social Cost of Monopoly

- 6.2.2 Calculating Deadweight Loss

- 6.2.3 Understanding Monopoly Regulation

- 6.3 Oligopoly

- 6.3.1 Introducing Oligopoly and the Prisoner's Dilemma

- 6.3.2 Understanding a Cartel As a Prisoner's Dilemma

- 6.3.3 Understanding the Kinked-Demand Curve Model

- 6.4 Monopolistic Competition

- 6.4.1 Defining Monopolistic Competition

- 6.4.2 Understanding Pricing and Output under Monopolistic Competition

- 6.4.3 Understanding Monopolistic Competition As a Prisoner's Dilemma

7. Resource Markets

- 7.1 The Derived Demand for Labor

- 7.1.1 Deriving the Factor Demand Curve

- 7.1.2 Deriving the Least-Cost Rule

- 7.1.3 Analyzing the Labor Market

- 7.2 Monopsony

- 7.2.1 Understanding Labor Market Power and Marginal Factor Cost

- 7.3 Capital Markets

- 7.3.1 Analyzing Capital Markets

8. Market Failures

- 8.1 Overview of Market Failures

- 8.1.1 Understanding Market Failures

- 8.2 Public Goods and Public Choice

- 8.2.1 Defining Public Goods

- 8.2.2 Analyzing the Tax System

- 8.2.3 Understanding Public Choice

- 8.3 Uncertainty

- 8.3.1 Understanding Expected Value, Risk, and Uncertainty

- 8.3.2 Understanding Asymmetric Information as an Economic Problem

- 8.3.3 Understanding Moral Hazards in Markets

- 8.4 Externalities

- 8.4.1 Defining Externalities

- 8.4.2 Explaining How to Internalize External Costs

- 8.4.3 Explaining How to Internalize External Benefits

- 8.5 Solutions to Externalities

- 8.5.1 Finding a Market Solution to External Costs

- 8.5.2 Finding a Negotiated Settlement to an External Cost

- 8.5.3 Applying the Coase Theorem

9. International Trade

- 9.1 The Basics of Open Economies

- 9.1.1 Determining the Difference between a Closed Economy and an Open Economy

- 9.1.2 Understanding Exports in an Open Economy

- 9.1.3 Analyzing a Change in Equilibrium in an Open Economy

10. Evaluating Market Outcomes

- 10.1 Normative Economics

- 10.1.1 Measuring the Benefits of Consumption

- 10.1.2 Using the Demand Curve As a Measure of Benefit

- 10.2 Calculating Total Economic Value

- 10.2.1 Quantifying Social Benefit

- 10.2.2 Quantifying Social Cost

- 10.2.3 Determining Total Social Cost

- 10.2.4 Understanding Economic Value

- 10.3 Consumer and Producer Surplus

- 10.3.1 Understanding Producer and Consumer Surpluses

- 10.3.2 Calculating Total Economic Value

- 10.4 Market Interference and Economic Value

- 10.4.1 Understanding the Effects of Price Controls

- 10.4.2 Understanding How Price Controls Destroy Economic Value

- 10.4.3 Evaluating the Effects of an Excise Tax

- 10.4.4 Assessing the Effect of an Excise Tax on Economic Value

- 10.4.5 Understanding How a Tax Can Create Deadweight Loss

- 10.5 International Trade and Economic Value

- 10.5.1 Evaluating the Gains from International Trade

- 10.5.2 Understanding the Effects of Tariffs on Consumer and Producer Surpluses

About the Author

Steven Tomlinson

Acton School of Business

Steven Tomlinson teaches economics at the Acton School of Business in Austin, Texas. He graduated with highest honors from the University of Oklahoma and earned a Ph.D. in economics at Stanford University. Prof. Tomlinson's academic awards include the prestigious Texas Excellence Teaching Award given by the University of Texas Alumni Association and being named "Outstanding Core Faculty in the MBA Program" several times. He has developed several instructional guides and computerized educational programs for economics.

Prof. Tomlinson is also an accomplished theater artist, with more than half a dozen award-winning solo performances to his credit. One play, Millennium Bug, presents a world in which all human interactions are strictly governed by economic calculations. His most recent play, American Fiesta, won the American Theatre Critics Association's Osborn Award for Best New Play by an Emerging Playwright.

In his Thinkwell presentations, Prof. Tomlinson uses his academic expertise and his stage presence to dispel the notion of economics as "the dismal science."

{kind=link}